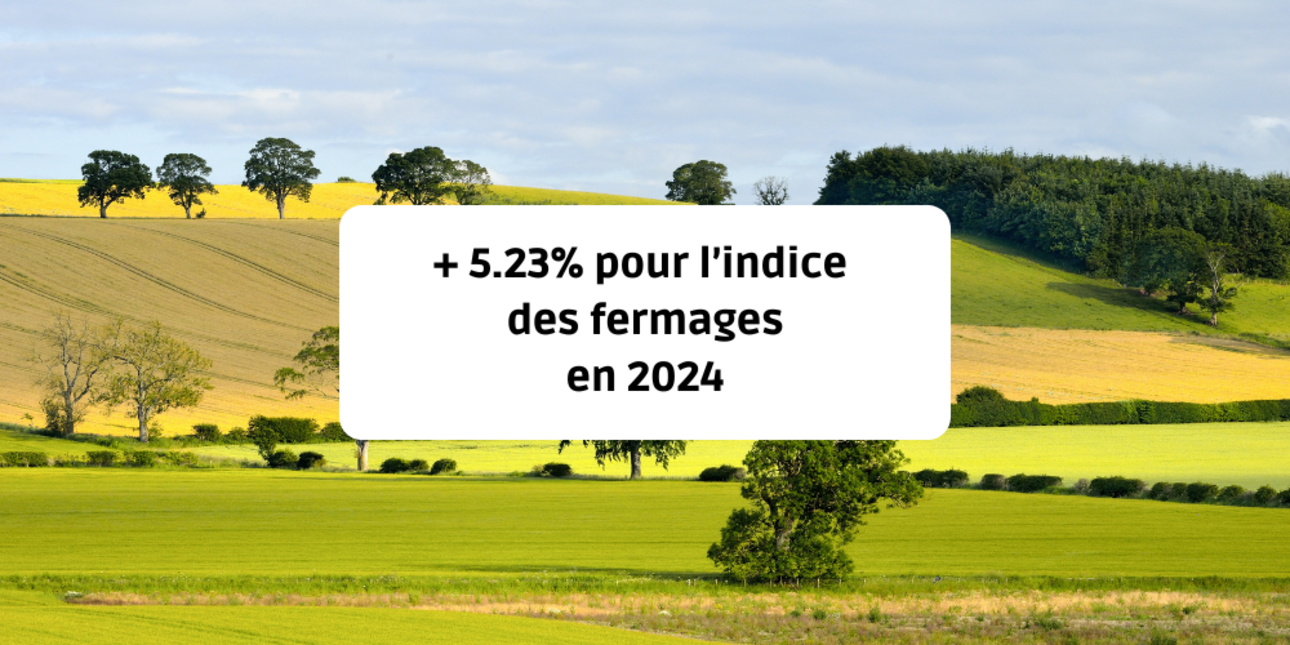

After a record year in 2023, the national farm index for 2024 has once again risen by an exceptional 5%.

The ministerial order of 17 July 2024, published in the Journal Officiel on 30 July 2024, set the index (at 122.55) used to calculate the increase in farm rents for rural leases for 2024.

As a reminder, the index is calculated from :

The index for farm rent reviews in 2024 is therefore 122.55, an increase of 5.23%.

| Year | Index | Change in index |

|

2009 |

100,00 |

Base |

|

2010 |

98,37 |

-1,63 % |

|

2011 |

101,25 |

+2,92 % |

|

2012 |

103,95 |

+2,67 % |

|

2013 |

106,68 |

+2,63 % |

|

2014 |

108,30 |

+1,52 % |

|

2015 |

110,05 |

+1,61 % |

|

2016 |

109,59 |

-0,42 % |

|

2017 |

106,28 |

-3,02 % |

|

2018 |

103,05 |

-3,04 % |

|

2019 |

104,76 |

+1,66 % |

|

2020 |

105,33 |

+0,55 % |

|

2021 |

106.48 |

+1.09 % |

|

2022 |

110,26 |

+3.55 % |

|

2023 |

116.46 |

+5.63 % |

|

2024 |

122,55 |

+5.23 % |

There are two calculation methods:

Calculation formula: Rent N = Rent N-1 x (1 + Index variation)

Example (1):

The rent on 1 October 2023 was €1,725.44.

On 1 October 2022, the rental price will be : 1,725.44 x (1 + 5.23%) = 1,725.44 x 1.0523 = €1,815.68.

Calculation formula: Rent N = Rent fixed in the lease x Index N/First index published after the lease was signed

Example (2)

The lease signed on 1 October 2010 stipulated a rent of €1,500.00. On 1 October 2022, the rent will be : 1 500,00 x (122,55/101,25*) = 1 815,55 €.

*The reference index is that for 2011, which was the first published after the lease was signed.

A number of factors also need to be taken into account when calculating the amount of the rent, including property taxes.

Landlords may ask their tenants for a partial refund of the property tax relating to the rented property.

The method of calculating this reimbursement must be specified in the lease agreement. If not specified in the contract, the tenant must reimburse his landlord :

Since 2006, agricultural properties have benefited from a 20% reduction in property tax, which must be passed on to the owner. In this situation, the lessee only reimburses the owner for the Chamber of Agriculture's share of the tax and the 8% administration fee.

If the share of property tax payable by the tenant under the rural lease is greater than 20%, the calculation should nevertheless be made by deducting this 20% reduction.

Property tax on agricultural land can be reduced or relieved, particularly for Young Farmers. When a landowner rents his land to a Young Farmer, a Young Farmer property tax rebate line may appear.

This reduction in property tax is not intended as a thank you to landowners who have leased their land to a young farmer. The landowner must pass on this saving to the tenant by applying an equivalent reduction to the tenant's rent bill.