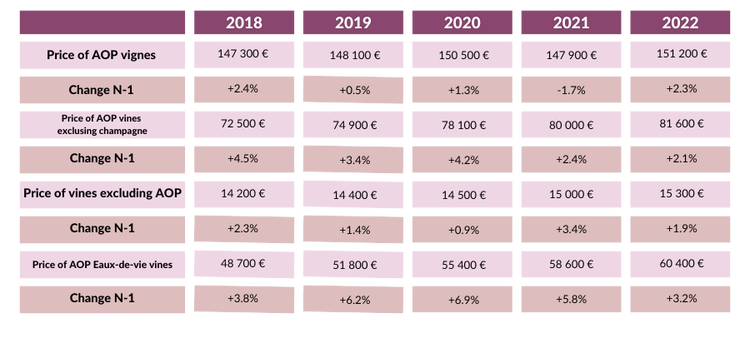

After a year of decline in 2021 (-1.7% to €147,900/ha), the price of PDO vines rose in 2022 by 2.3% to €151,200/ha. We analyse the figures provided by the SAFER for you (Analysis of rural land markets - June 25, 2023).

The vineyard market is highly heterogeneous, and it is useful to divide sales according to the type of vineyard: vines with a Protected Designation of Origin, vines outside Protected Designations of Origin, and vines intended for the production of eaux de vie (Cognac, Armagnac, etc.).

Given the very specific market for vines in Champagne, the price of PDO vines is also calculated outside Champagne.

Source: SAFER - Analysis of rural land markets - June 25, 2023

We are therefore seeing an increase in the price of PDO and non-PDO vines, as well as for brandy vines.

We also note that cumulative inflation from 2018 to the end of 2022 is 10.6%. The average increase in the sale price of PDO vines over the same period (+2.6%) is therefore insufficient to protect the value of the estate.

Excluding Champagne, the selling price of PDO vines has risen by 12.5% since 2018 and has therefore increased in value by slightly more than inflation.

On the other hand, prices for AOP Eaux-de-vie vines have risen significantly, by 24% since 2018, driven by the Cognac vineyards (see prices by vineyard).

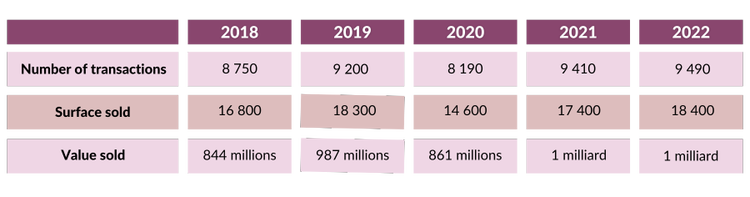

The number of transactions recorded by SAFER in 2022 reached a record high of 9,490, up 1.1% on 2021.

The number of land sales had plummeted in 2020, but rebounded logically in 2021. It is therefore always difficult to compare figures from one year to the next.

If we compare the volume of sales with 2019, the increase is real but smaller:

Source: SAFER - Analysis of rural land markets - June 25, 2023

Sales to farmers fell sharply, by 3.6% in number of transactions and by 11.3% in surface area sold.

Sales to non-farmers (individuals) also fell sharply, both in terms of number of transactions (-4.6%) and surface area (-15.1%).

Sales to companies rose sharply in number (+6%) and surface area (27.5%).

The use of companies to hold land has been on the increase for many years. It is primarily a response to entrepreneurial objectives: separation of land assets from business and private assets, the need to raise outside capital, partnerships between winegrowers, preparation for transfer within or outside the family, etc.

Sales of land (agricultural or wine-growing) to companies have been rising sharply for some time. Sales of shares in these companies (on which SAFER's pre-emption rights are limited) have also been on the increase for several years.

Source: SAFER - Analysis of rural land markets - June 25, 2023

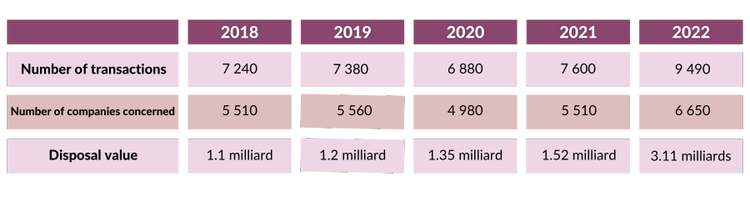

The number of transactions involving agricultural companies has therefore exploded (+25% compared with 2021 and +28% compared with 2019).

In value terms, the increase is even greater (+105% over 1 year and +259% since 2019).

The forthcoming implementation of the Sempastous Law, which will enable SAFER to monitor sales by agricultural companies, partly explains this sharp increase.

However, this factor needs to be qualified for several reasons:

The increased use of agricultural companies has been an ongoing trend in agriculture for a very long time, as they offer a number of advantages: ease of transfer, tax and social optimisation, protection of private assets, status of spouses, grouping together of farmers, etc. It is therefore logical that shares in these companies should be sold a few years down the line.

Not all agricultural companies own land

The market for shares represents 7.9% of the number of transactions, which is relatively low

Only 41% of sales of shares in agricultural companies are to new partners who are not related to the seller. The remainder were sold to partners already present in the companies or to members of the seller's family.

We will shortly be taking a closer look at price trends in our articles devoted to each vineyard, for which we have included the values since 1991.

In this section, you will find an overview of price trends by vineyard.

The average price of vines in the Alsace-Est vineyards will be 1.3% higher in 2022 than in 2021. In particular, there will be a 6% increase in Bas-Rhin (€90,500/ha), compared with a 1% fall in Haut-Rhin (€130,000/ha).

This increase does not make up for the loss of value in recent years.

Although the number of transactions is down significantly (-5.5%), the surface area involved is 30% larger than last year.

At €114,000/ha, the average price of vines in the Bordeaux-Aquitaine region is 3% lower than in 2021.

In Gironde, a vineyard currently in crisis, the fall is 3% to €127,900/ha. At the same time, prices are up in Dordogne (+6% to €10,400/ha) and Lot-et-Garonne (+7% to €13,600/ha).

The number of transactions is down (-1.9%), as is the overall surface area sold (-1%).

The average sale price of vines rose sharply by 9.4% to €220,900/ha.

The dynamism of prices is also reflected in volumes, with the number of transactions on the rise (+3.9%), as is the surface area sold (+3.4%).

The increase is particularly strong in Burgundy, with a 12% rise in Côte-d'Or to 887,200 €/ha.

After 3 years of decline, the market for Champagne vines is regaining momentum:

Prices rose by 3% in Aisne (€840,100/ha), Aube (€897,300/ha) and Marne (€1,159,000/ha).

The price of Eaux-de-vie PDO vines continues to rise, by 3.2% to €60,600/ha. While prices remained stable in Charente-Maritime (€60,800/ha), they rose by 6% in Charente (€60,400/ha).

However, the number of transactions and the surface area sold fell sharply (by 6.3% and 13.3% respectively).

The price of PDO vines fell by 7.7% in Corsica, while the price of non-DPO vines rose by 20% to €18,000/ha.

However, prices remain difficult to estimate given the low number of transactions (10, down 23.1%) despite the increase in the surface area sold (+135.5% with 100ha).

The price of PDO vines rose by 1.4% to €13,000/ha, but remained lower than that of non-DPO vines, which rose more rapidly (+3.7% to €15,600/ha).

The number of transactions fell by 4.3%, while the surface area sold increased slightly (+1.8%).

The price of non PDO vines in the Hérault region rose by 6% to €16,800/ha.

The wine market was buoyant in 2022 in the South-West vineyards. The price of PDO vines rose by 7.9% to €14,000/ha, while the price of non-DPO vines remained virtually stable at €12,800/ha (+0.9%).

The area sold rose sharply (900ha +32.7%), with a slightly higher number of transactions (190 +2.8%).

The biggest increases were in Lot (+35% to €14,600/ha) and Aveyron (+11% to €21,000/ha). The other départements are stable or slightly up.

The market in the Loire Valley is also very buoyant, with prices up 11.1% to €39,200/ha for PDO vines. By contrast, prices for non-DOP vines remained stable.

The area sold is up (+26.4% to 2,300 ha), as is the number of transactions (+10.8% to 1,560).

It is in the Cher department (Sancerre in particular) that prices have risen the most, by 22% to €214,200/ha.

The average price of vines remained virtually stable at €51,800/ha (+0.8%) in a fairly buoyant market, with 2% more transactions (1,400) and 12.9% more surface area sold (3,000ha).

The vineyard sales market is therefore set to be very buoyant in 2022, with record volumes and sharply rising prices. Prices vary by vineyard and appellation, of course, and will be the subject of separate articles.

Source: SAFER - Analysis of rural land markets - June 25, 2023 (and previous years)